Banking is the only industry where you intimidate your customers. And treat both customers (loan takers) and suppliers (depositors) like dirt. Because of the right you have from regulatory capture. When the bank goes under, forget what documents say – the govt has to bail out the account holders.

So each deposit taking bank is a risk to the govt and to the central bank. And a big bank is a systemic risk like no other. A couple of months ago I had posted that HDFC has to be split to reduce this risk. And that the merger with HDFC Ltd was a regulatory blunder.

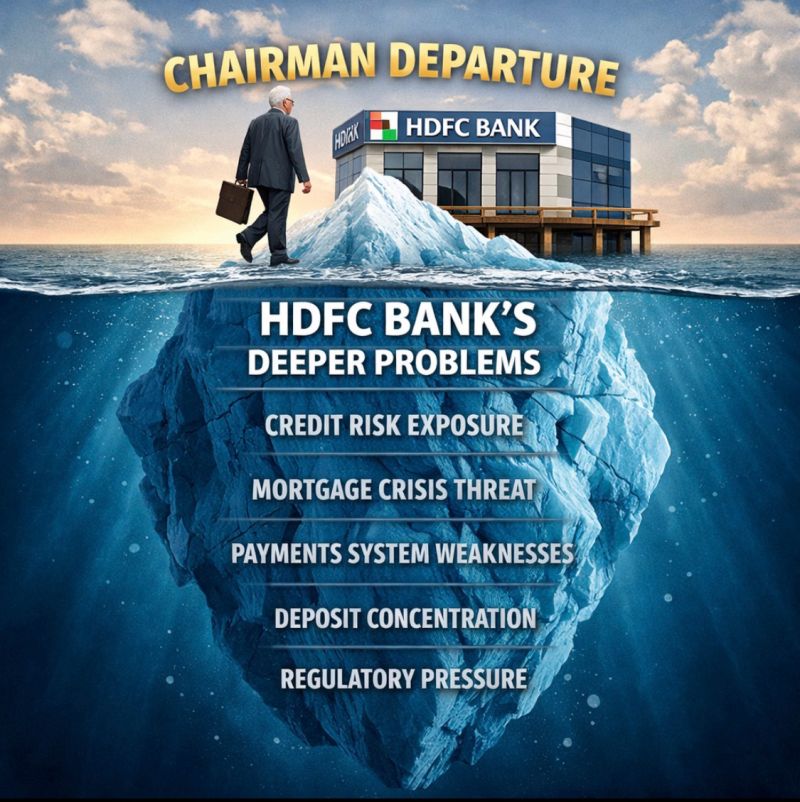

The departure of the chairman at HDFC Bank is being discussed as a major leadership event. But in reality, it may only be the visible tip of a much larger iceberg. There are just too many bad actors in the Bank to be rectifiable by merger with the Kosher HDFC.

The merger with Housing Development Finance Corporation created a balance sheet of extraordinary scale — deeply embedded in mortgages, retail credit, corporate lending and the country’s digital payments infrastructure. It has become the prime proponent of the real estate and luxury car bubble. A country as poor as India is buying Rs 100 cr apartments and Rs 5 crore cars as if it was the prime beneficiary of the AI bubble.

When an institution reaches that size, leadership transitions are rarely just about individuals. They often signal deeper structural pressures: integration challenges, deposit competition, regulatory scrutiny, technology outages, and the complex task of managing one of the world’s largest housing loan books.

In finance, the visible event is often the smallest part of the story.A leadership change is simply the first signal that larger questions are being asked beneath the surface.

98% of the public FDs by value have been distributed as loans. This means that to redeem old FDs, they have to issue new FDs. The loans are for 3 year or 5 year tenures. fDs are of shorter tenure.

The salaried class are the prime customers of the bank. They give Fds, keep large savings account balances, take housing /car loans and pay 5% pm interest on a credit card. Many of them will soon lose their jobs to AI. The credit rating paradigms which justified these loans are no longer valid. The collateral against which these loans were given is junk. You can’t dispose off a thousand houses in Gurgaon at Malabar Hill prices for cash. It is a make belief price created by them in a conspiracy with the builders.

SBI or PNB or BoB are far superior to HDFC – in both loan book diversity and nation building. They actually fund job creators and msme players. They fund industry and infrastructure. HDFC on the other hand meets priority sector lending quotas by showing luxury car loans as msme lending. Or by giving overdraft accounts against FDs. It is the havala bank playbook.

There is poor cybersecurity. IT malfunctions. Money disappears during auto sweeps. Yet they have market dominance.

It is not if, but when it will all blow up.