There is nothing ethical about how shares are sold to the public in a India. The general paradigm is “buyer beware” and the only onus on the issuer is “disclosure”. Which means that there are a couple of relevant paragraphs hidden in 650 pages of a document called a DRHP.

There are several schools or mismanagement that are prevalent. One is the Anil Ambani school. Here the promoter buys shares for par in a new group company in their personal names – and then the company buys some at a premium – and then the hope is that the public will buy at a super premium. And the original promoter will take out his money as soon as the public money comes in. There are various variants of this broad principle. But the gold standard is what the foreign banks like Citibank do. They keep merging, emerging, slump selling, transferring, revaluing …. Etc till no one has a clue as to what happened, when and to whom. The regulator gives up after a while and the scheme goes through.

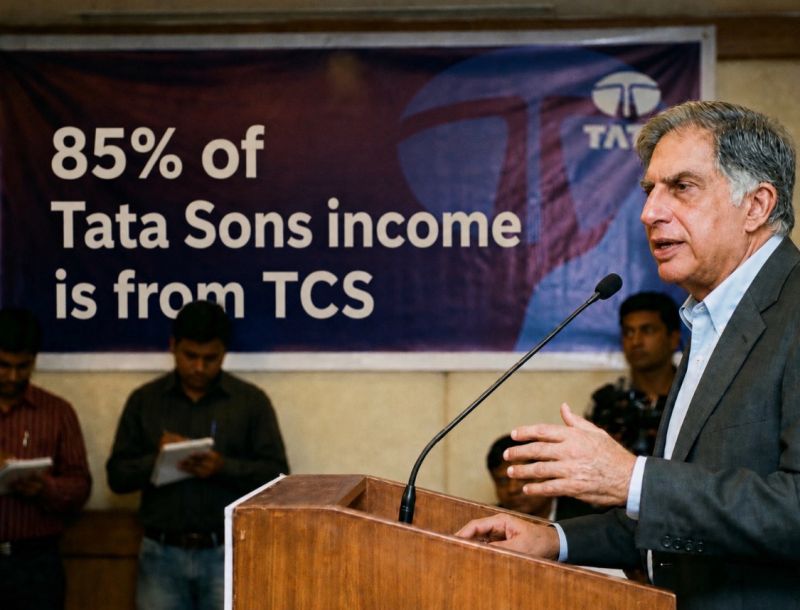

Now if the approach is clean and honest – you have a problem. It is all very nice to say that you will invest Rs 500,000 crores in a semiconductor plant – except for that there is no money to actually invest.

Thus the only way out for the Tatas is to change to a AIF structure so that they can access dumb money which takes an economic interest but does not take any control. AIFs call this LP capital and the Tata Trusts can be sponsor or GP capital. This money comes on a profit share basis and the investors will take away 80% of the gain (assuming it is a 2 and 20 aif). However there is no interest involved and no repayment.

Given that the Tatas have purchased their own noose around their neck by buying Air India – this is really their only option. What they can also do is to transfer their air India holding to a air India holdings Ltd and seek some form of grant or subsidy from the govt. They took a Rs 40,000 cr pa loss off the books of the govt – that some kid of help is well deserved. They can give the Padma Bhushan back and say “sorry we made a mistake”. This has enough precedence. Vodafone is seeking sops to survive and no one did pay the fancy figures that they quoted for telecom licenses on the 1990s.

The bigger issue for the Tatas is what to do.

It is fairly easy to figure out what not to do. Everything that Chandrasekhar did is in that category. Apple contract mfg is a high top line disaster. Trying to manufacture Airbus planes is hilarious. The semiconductor fab will never make short term sense in India unless you do something simple like make solar cells from sand. The market is real. As well as protected. Making fancy chips In a USD 10B lab is very nice for the equipment suppliers. Not for Tata. It may be nice for the country if we can find buyers for the chipsets.

I really don’t see why anyone will buy chips from a Tata or L&T. These cos have no clue about this business.