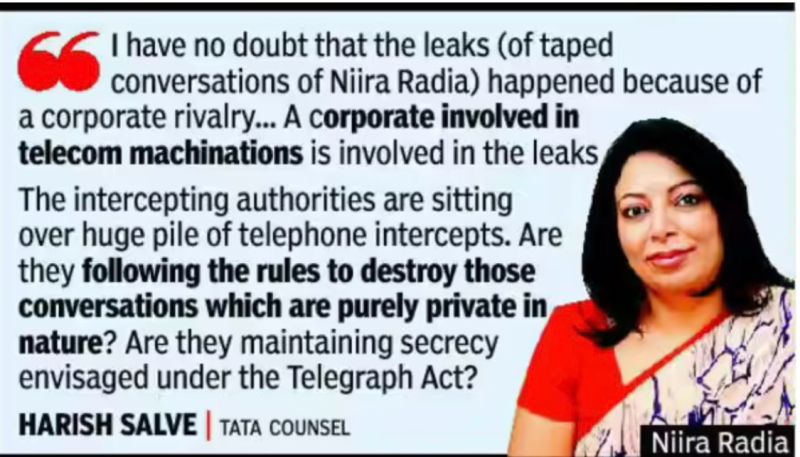

Chapter 11G: In 2010, a writ was filed in the Supreme Court by Ratan Tata seeking a stay on the release of the controversial 5800 recordings on Nira Radia. Like Mr Salwan was a legal luminaire for Citibank, Ms Radia was a management genius for Tatas. So much so that the Tatas paid her Rs 56 crores or some such amount pa as consultancy and advisory fees. Prior to becoming a consulting genius, she worked as a liaison officer for Sahara. Something I will revert to later in the context of the post on the destruction of Sahara.

Now what were these tapes. Here is what Google returns:

To avoid any noise, let me add a link to a Supreme Court order available online which is self explanatory.

This is the order passed by Justice Singhvi in the order.

What the order does not reveal is the individuals and entities involved. Prashant Bhushan tried to get these declared publicly. But given the highly delicate nature of subjects – and especially because it concerned the judiciary and its internal workings – the tapes never did go public.

But not much is left to the imagination on who it involved and why. It all keeps going back to Pramit Jhaveri, Tatas, L&T, Shadow banking, HDFC, Citibank.

The Citibank legal structure in India has always been brilliant. All entities were focused on the dual paradigms of “collect and export”. So when LG and Hyundai wanted to sell shares in their subsidiaries to retail investors and export the proceeds – there was only one merchant banker good enough for the role. The category 1 merchant bank has raised over Rs 300,000 crores for the likes of LG and Hyundai ipo.

Now try setting up a company in Korea as an Indian – and then unloading the shares to ill equipped retail investors in Korea – to export the proceeds to India. Or try doing this in China or in say UK. No chance.

Of course all of this raises a really fundamental issue. Can scarce savings of poor and middle class Indians be diverted to funding foreign companies who will use this money to kill Indian competitors.

Who approves these valuations ?? And why. How can the valuation of LG India be more than that of its principal in Korea. Remember LG India was a 100% subsidiary of LG Korea.

The subject of valuations by Citi can open up a super market of worms. HDFC historically traded at a price to book of 4. SBI historically was at 1. It needs to be understood that when a bank gives a loan, there is no upside, only downside. Either the loan will come back or will need a write off. It doesn’t ever happen that a borrower repays 2-3x of the loan. He will only pay back the principal. That is why at steady state equilibrium the price to book will be between 1 and 1.5. In venture capital however you could get 5x or even 100x.

So info edge (India’s largest domestic VC) at a price to book of 1.5 and Tata Capital at 3 ….. is well !!!